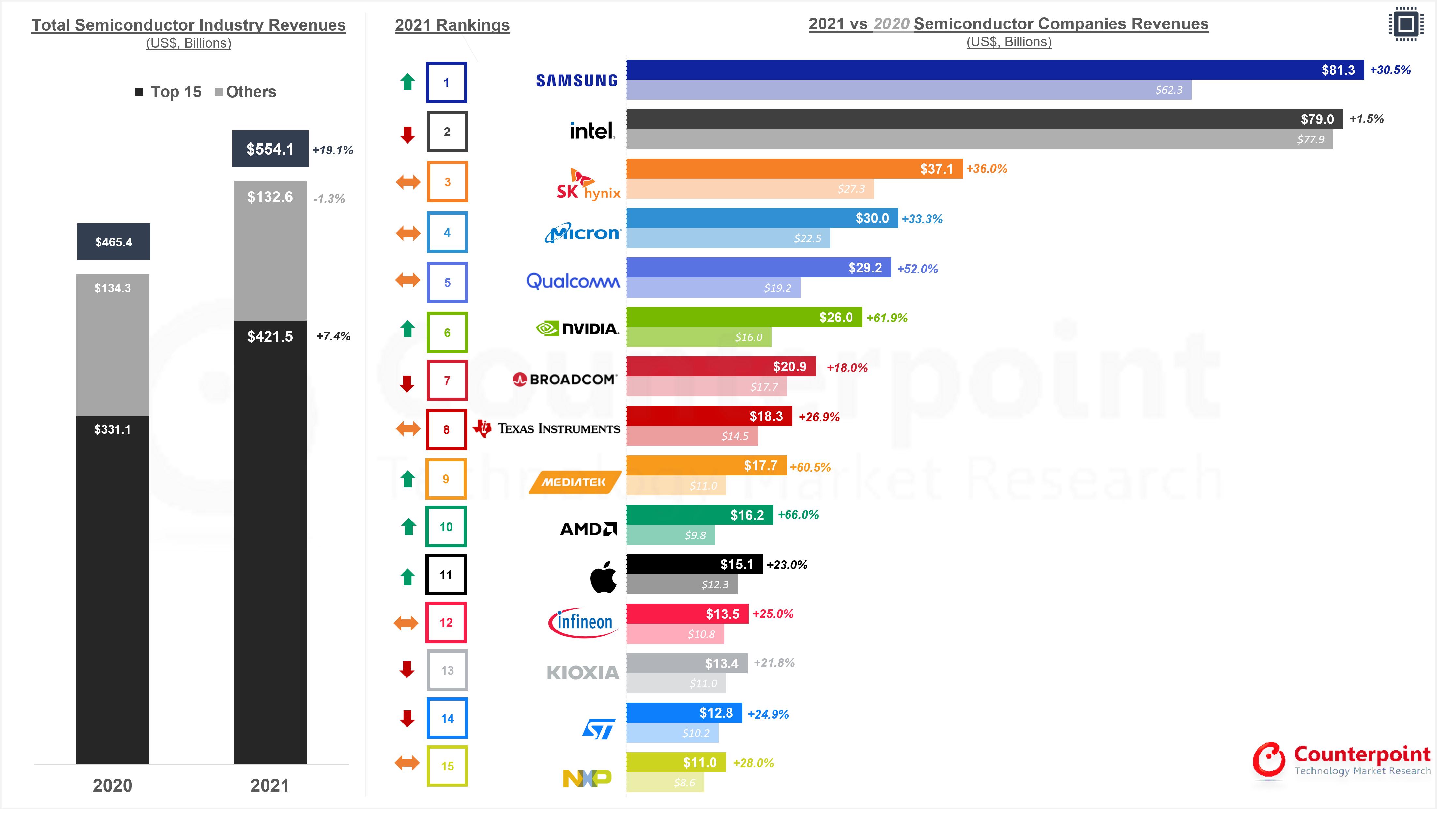

Semiconductor industry went through significant structural changes in 2021 after entity lists were announced by both China and the US. The overall 2021 semiconductor revenue rankings also varied from the previous year. Samsung took the first position from Intel thanks to its solid growth momentum in both logic IC and memory segments. Memory vendors continued to lead the industry with SK Hynix and Micron taking the third and fourth positions, followed by IC design vendors, including Qualcomm and NVIDIA.

During 2021, many top-tier semiconductor companies reiterated material changes happening in the industry, such as semi content growth, higher inventory level and longer chip lead time due to global component shortages as well as logistical issues. The year saw 19% YoY revenue growth with the largest contribution coming from the memory and IC design sectors.

Semiconductor Industry Top Players Revenues & Rankings – 2021

Samsung took the lead in 2021 with a strong DRAM and NAND flash market performance at the expense of Intel’s relatively flattish results. Major smartphone SoC and GPU vendors also enjoyed strong growth in the year with over 50% YoY revenue increase. In addition, we saw 27% YoY revenue growth among the top 15 vendors, outperforming global semiconductor revenue growth and implying another year of centralised semiconductor industry.

In general, we believe supply constraints will likely persist before H2 2022, though our checks suggest some amount of component shortage easing. Looking ahead, foundries are adding new capacities in 2023 and most of them hold optimistic views on their partnerships and utilization rates even if supply and demand normalise in the foreseeable future. High performance computing, metaverse (AR/VR/XR), 5G and automotive remain key semi content growth drivers for the industry.

{kind=link}